Introduction and Current Market Scenario of the Automotive Powertrain Industry

The automotive powertrain market, which encompasses all components that create and transfer power to a vehicle's wheels, is a key player in improving vehicle performance, fuel efficiency, and emissions control. The market is undergoing a significant transformation with the increasing demand for electric and hybrid vehicles, leading to a focus on innovative technologies like electric motors and battery systems. Importantly, regulatory requirements aimed at reducing emissions and increasing fuel efficiency are driving substantial innovation in powertrain design. As a result, the automotive powertrain market is expected to witness significant growth as manufacturers adapt to changing consumer demands and environmental standards.

Cognitive Market Research noticed that the demand for Automotive Powertrain in a variety of industries, including automotive, aerospace and defense, construction and agricultural equipment, is the primary driver of significant growth in the global Automotive Powertrain market. The Automotive Powertrain market was estimated to be worth approximately USD 812451.2million in 2024 and is projected to increase to USD 2892132.447 million by 2032, with a compound annual growth rate (CAGR) of 17.20% during the forecast period, according to a recent market analysis. Arval, a well-known car leasing and mobility solutions provider, announced a strategic relationship with BYD (Build Your Dreams), a global leader in electric vehicle production. This organization, established through a Memorandum of Understanding (MoU), demonstrates Arval's commitment to improving its electric vehicle (EV) rental contributions for business fleets and individual clients.

What are the current trends of the Automotive Powertrain Market?

Based on the research conducted by Cognitive Market Research, the global Automotive Powertrain market is estimated to be worth approximately USD 812451.2 million as of 2024. This market size is indicative of strong demand in a variety of sectors, with a particular emphasis on automotive, aerospace and defense, construction, and agricultural equipment. The market value has been substantially influenced by the growing use of powertrains in various industries. The market is anticipated to expand at a compound annual growth rate (CAGR) of 17.20%, with a market value of approximately USD 2892132.447 million by the conclusion of 2032. The growing demand for vehicle electrification in the automotive sector, as well as increased sales of electric vehicles, all contribute to the demand for automotive powertrains. Furthermore, the growing need for automated transmissions and engine downsizing to increase vehicle fuel efficiency is expected to drive market expansion.

North America accounted for approximately 35% of the total market in 2023, constituting the largest market share in the global Automotive Powertrain market. North America has increased demand for modern powertrains that are lower in weight, improve fuel efficiency, reduce emissions, and enhance vehicle performance.

Europe follows with a 30% market share, the rapidly developing market for automotive powertrains in the region can be ascribed to rising demand for electric vehicles as a result of carbon pollution rules enacted by the European Union and respective national governments. The Asia-Pacific region is experiencing accelerated growth, with approximately 25% of the market held by countries such as China and Japan. This is a result of their heightened emphasis on innovation and their expanding industrial base. The Asia-Pacific market share is anticipated to increase to 29% by 2024, representing the highest CAGR among all regions, with a rate of 12%. The accelerated industrialization and the increasing adoption of advanced powertrains in manufacturing and machinery are the driving forces behind this growth.

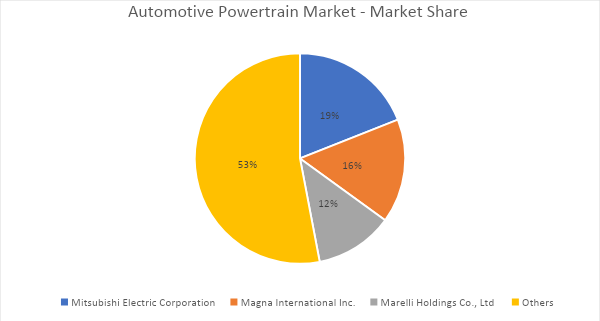

The Automotive Powertrain market is intensely competitive, with several prominent competitors monopolizing the landscape. Mitsubishi Electric Corporation, Magna International Inc., and Marelli Holdings Co., Ltd. are among the most significant organizations. Mitsubishi Electric Corporation maintained a dominant market share of approximately 19% in 2023, with Magna International Inc. and Marelli Holdings Co., Ltd following at 16% and 12%, respectively. These organizations are consistently investing in research and development to enhance and innovate their product offerings, thereby preserving their competitive advantage. Mergers, acquisitions, and strategic partnerships are also indicative of the competition, with the objective of broadening product portfolios and global reach. New entrants and increased competition are anticipated in the competitive landscape by 2024, with a particular emphasis on emerging markets in the Asia-Pacific region.

The all-wheel-drive system delivers power to all wheels to increase the car's traction and handling. Especially while turning, the system distributes torque evenly to all four wheels, giving the car more traction and grip. The recent advent of all-wheel drive (AWD) systems in compact passenger cars and hybrid vehicles has helped to expand the market under research. Previously, only expensive cars could use this technology. Premium and high-end cars are in high demand in the Asia-Pacific automotive all-wheel-drive market, owing to increased consumer expenditure in emerging nations such as China and Japan. Improved safety, stability, fuel efficiency, and driver control are a few other advantages that may propel the demand for automobile powertrain systems.

Technological Trends and Advancement in Automotive Powertrain Market?

Technological developments in the automotive powertrain market are improving vehicle performance, fuel efficiency, and emissions control. Electrification is a key trend, with automakers rapidly integrating electric powertrains, such as battery electric vehicles (BEVs) and hybrid systems, to fulfill global emissions limits. Advanced transmission systems, such as dual-clutch transmissions (DCT) and continuously variable transmissions (CVT), enhance driving dynamics and fuel efficiency. Another significant breakthrough is the rise of turbocharging and engine downsizing, which enable smaller engines to give more performance while being more efficient. Additionally, lightweight materials such as aluminum and carbon composites are being used to reduce vehicle weight, hence improving fuel efficiency and powertrain performance. Geely and Nio, Chinese manufacturers, have formed a strategic cooperation to focus on battery-swapping technology. The understanding entails comprehensive collaboration that includes battery rules, battery swapping technology, the expansion and activity of battery swapping organizations, the advancement of swappable models, and the management of battery resources.

The Asia-Pacific market is undergoing the most rapid development, which is attributed to the rapid industrialization and technological advancements in countries such as South Korea, Japan, and China. As of 2023, the Asia-Pacific region accounts for 29% of the global AOM market. This figure is anticipated to rise to 28% by 2024, indicating a compound annual growth rate (CAGR) of 12%. This expansion is primarily due to the growing manufacturing sector and the increased investment in research and development. North America continues to be the most significant market, possessing 35% of the global market share, as a result of its substantial investments in research and development and advanced technological infrastructure.

Development of Fuel-Efficient Vehicles as one of the key Opportunities for the Automotive Powertrain Market

There is a growing need for cars that are more emission- and fuel-efficient-free due to rising fuel prices and environmental sustainability concerns. Hybrid powertrains, electric powertrains, and turbocharged engines are becoming increasingly popular because they provide better fuel economy and lower pollution. With the growing demand for electric and hybrid vehicles, the automotive powertrain business is expanding dramatically. Electric powertrains have various advantages over traditional combustion engines, such as higher efficiency, lower pollutants, and cheaper maintenance costs.

In 2023, the automotive powertrain market saw a significant increase in adoption across various industrial sectors, including automotive, aerospace and defense, construction, and agricultural equipment. The automotive industry, in particular, has been a key driver of this growth, using automotive powertrains to enhance product quality and increase efficiency. This is evident in the fact that the automotive segment accounted for approximately 40% of the total automotive powertrain market revenue in 2023, as per recent market data. The shift towards electrification and fuel efficiency is fueling the demand for vehicle power systems, with consumers seeking increased performance, better fuel economy, and lower pollutants. This trend is driving the popularity of electric vehicles (EVs) and hybrid electric vehicles (HEVs), leading to increased demand for advanced powertrain systems such as electric motors, battery systems, and regenerative braking technologies.

The aerospace and defense segment of the automotive powertrain market experienced a remarkable 12% growth in 2023; the demand for automotive power systems centers on high-performance, long-lasting powertrains that can function in harsh situations. Ground vehicles, such as military trucks and transport vehicles, rely heavily on power systems that are reliable, efficient, and high in torque. Defense organizations are increasingly turning to hybrid and electric power options to minimize fuel consumption and improve fleet sustainability.

The Automotive Powertrain market is poised for future growth in the construction and agricultural equipment sector. In 2023, this segment experienced an 8% growth rate, indicating a steady increase in adoption. There is a growing demand for fuel-efficient and environmentally conscious power systems, particularly with the push for cleaner diesel engines and electric powertrains in heavy-duty gear such as tractors, excavators, and loaders. Hybrid and electric power systems are being used to reduce operating costs, pollutants, and noise while increasing performance. The use of autonomous and semi-autonomous equipment in construction and farming is driving the demand for improved powertrain systems that are efficient, long-lasting, and responsive to intelligent control systems.

Expensive Production Costs to Hinder the Market Growth

Expensive production costs provide a significant problem in the automotive powertrain business, owing to the integration of modern technologies and materials. The drive to electrification has resulted in the creation of electric powertrains, which require high-cost components such as batteries, electric motors, and power control units. Furthermore, lightweight materials like aluminum and carbon composites, which are utilized to improve fuel efficiency and reduce emissions, drive up production costs. The development and production of hybrid and advanced internal combustion engines (ICEs), which include features such as turbocharging, downsizing, and improved transmission systems, are also expensive due to the requirement for precision engineering and high-performance components. R&D expenses to fulfill rigorous emission requirements and improve efficiency increase the overall production cost. These aspects, together with the necessity to scale up production to meet growing demand, make it challenging for automakers to balance performance, efficiency, and cost-effectiveness in the powertrain market.

Another significant challenge in the automotive powertrain sector is the development and integration of advanced powertrain components such as e-drives, transmissions, batteries, and fuel cell powertrains. These tasks pose substantial technical hurdles that will significantly shape the future of the automobile powertrain market. Engineering teams are confronted with the daunting task of developing systems that are not only efficient and reliable but also cost-effective and scalable for mass production. Each component, from battery technology advancements for longer ranges to fuel cell integration for faster refueling times, demands substantial R&D investment and innovation.

Expected Future Developments in Automotive Powertrain Market

The automobile powertrain market will undergo a major transition in the next years owing to technological developments, regulatory pressures, and altering consumer preferences. As the global desire for lower emissions and higher fuel efficiency grows, electric vehicles (EVs) and hybrid powertrains will gain market share. Automakers are putting more emphasis on developing battery electric cars (BEVs), plug-in hybrid electric vehicles (PHEVs), and fuel cell electric vehicles (FCEVs). The improvement of battery technology, particularly in terms of energy density and charging speed, will be critical to the mainstream adoption of electric powertrains faster refueling compared to battery-electric solutions, and research into hydrogen powertrains is likely to expand significantly in the coming years. Hydrogen fuel cells are projected to play a significant role, particularly in commercial vehicles and long-haul trucks. Fuel cells provide the possibility for extended ranges. For example, Geely and Renault Group engaged into a joint venture deal, with each holding a 50% interest in the new firm. The fundamental goal of this collaboration is to achieve supremacy in the market for next-generation highly efficient and hybrid powertrain solutions in response to the projected worldwide demand in coming years. Renault Group and Geely intend to combine their knowledge, resources, and technical breakthroughs to meet the changing needs of the automotive industry.

Despite the increase in electrification, advanced ICE technologies will continue to progress, especially in the short to medium future. Turbocharging, engine downsizing, and increased thermal efficiency are some of the developments targeted at making ICEs more fuel-efficient and comply with rigorous pollution standards. These advancements will help ICE-powered vehicles remain competitive, especially in areas where electric infrastructure is still developing. Future powertrain systems will become more integrated with smart technology, utilizing IoT and artificial intelligence to improve performance, energy economy, and diagnostics. Predictive maintenance based on data from connected systems will reduce downtime and extend the life of powertrains. A greater emphasis on sustainability will encourage the adoption of recyclable materials and environmentally friendly manufacturing procedures in engine components. The creation of lightweight materials such as carbon composites and aluminum will also continue to improve vehicle efficiency.

Conclusion

At this juncture, the automotive engine market is undergoing a fundamental instability, fueled by technical developments, environmental laws, and shifting consumer preferences. Traditional internal combustion engine (ICE) powertrains, which were once the industry standard, are being reinvented using turbocharging, engine downsizing, and hybridization to meet stricter emission limits and improve fuel efficiency. However, the future of the powertrain sector rests in electrification as electric vehicles (EVs) and hybrid electric vehicles (HEVs) achieve mainstream adoption. Electrification is at the heart of this transformation, with battery electric cars (BEVs) and plug-in hybrid electric vehicles (PHEVs) gaining popularity due to their lower emissions and increased efficiency. The continuing advancement of battery technology, including advances in energy density, charging speed, and cost reduction, will expedite the shift.

Despite the increase in electrification, sophisticated ICE technologies will continue to play a role in the short to medium future, particularly in areas with insufficient electric vehicle infrastructure. Innovations in turbocharging, fuel efficiency, and thermal management will keep ICE powertrains competitive but at a lower capacity. The integration of smart technologies and connected systems is also expected to transform the powertrain industry. IoT-enabled powertrains will offer real-time performance data, predictive maintenance, and increased efficiency, while autonomous driving technologies will fuel demand for intelligent, high-performance powertrains.

Author's Detail:

Kalyani Raje /

LinkedIn

With a work experience of over 10+ years in the market research and strategy development. I have worked with diverse industries, including FMCG, IT, Telecom, Automotive, Electronics and many others. I also work closely with other departments such as sales, product development, and marketing to understand customer needs and preferences, and develop strategies to meet those needs.

I am committed to staying ahead in the rapidly evolving field of research and analysis. This involves regularly attending conferences, participating in webinars, and pursuing additional certifications to enhance my skill set. I played a crucial role in conducting market research and competitive analysis. I have a proven track record of distilling complex datasets into clear, concise reports that have guided key business initiatives. Collaborating closely with multidisciplinary teams, I contributed to the development of innovative solutions grounded in thorough research and analysis.